Solv Talk | Uniswap V3—Is NFT the only way to upgrade DeFi?

Mike Meng : The Uniswap V3 was released today, I can see that there’s a lot of hype for it, with many people believing that Uniswap V3 will be a game changer in the AMM field. Zhiqiang, you have been tracking all kinds of innovative products in the field of DeFi, what do you think of Uniswap V3?

Ryan Chow: The V3 scheme that Uniswap released recently has a lot of highlights, including a Layer2 solution, a rich market-making mechanism, an optimized oracle program and more. However, its biggest breakthrough is not the Layer2 scheme that many people expected, but rather the use of NFT to replace the original ERC-20 LP Token. This is the boldest innovation in the entire new upgrade, it is also the foundation for realizing V3’s high-level Market Maker Rule.

From the perspective of functions, market makers can choose to centralize the liquidity within a certain price range. In the past, the money from market makers was distributed between 0 and infinity, but now, the same money can be effectively centralized in a range, which will greatly improve the utilization of the funds. One of the best examples is the trading between stablecoins tends to have smaller price fluctuations, and market makers can make markets around the 1% range with ranges up and down of 1:1. By this means, the same 1 million U.S. dollars will play a market making effect of 200 million U.S. dollars, imagine how powerful it will be.

This innovative direction is not very difficult to imagine. Naturally, we would provide the users with more diversified market making choices, and at the same time improve the utilization of funds throughout the entire pool. This is not an unsolvable issue from the perspective of the code. If this is the case, then why was it that Uniswap did not propose this innovative direction until half a year after DEX became so popular?

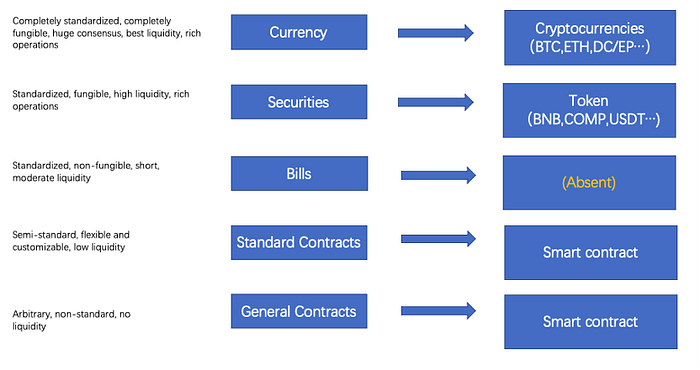

The key point is that the team needs to break through the mindset of taking ERC-20 as the LP Token in order to open up new space. In essence, the LP Token describes the contract between the user and the platform, the advantages of adopting ERC-20 are for its homogenization, free splitting and its strong mobility, however, its major disadvantage is the poor information description options. This results in the limitations from the ERC-20 to the platform when providing the users with functional choices, for example, most of the DEX currently can only provide the market making of an entire curve, only current lending in the lending products, and only sustainable products in the derivatives, essentially, they are restricted by the functions of the ERC-20.

Mike Meng : If it is as you say, I think the Uniswap V3 will greatly advance the application of note token in DeFi. Of course, we are very happy about this, as we have chosen the direction of note token more than half a year ago as our team’s main focus in the DeFi innovation. What we have considered at the time has all been reflected in the article “What are digital assets”, which was published last October. According to our observation, in the real world, the consumer goods in the real economy are basically not homogenous, they are different from each other and are unable to split. While in the virtual economy, many of the financial products are homogenous, as they are the shared expression of the abstract concept of value. For note, it is a significant bridge connecting the real economy to the virtual economy, capable of recording the customized contractual relationship, and it projects the non-homogenous consumer goods into the splitable and composable financial contracts, achieving balance in the liquidity and descriptiveness. Therefore, for real economy, note is the key to the financial transaction market, for virtual economy, it is an image of the assets in real world, it is never too overemphasized to mention its significance. I believe that in the decentralized world, the products which are similar to the notes are needed as the link to realize the value flow.

Will Wang : As the matter of fact, from the perspective of DeFi’s own development law, the more complex financial demands would correspondingly require financial products with a higher order and multi-dimensional properties. As the assets held by each user becomes increasingly differentiated, it is natural that the tokens corresponding to these assets are unable to be 100% homogenized with each other. This has also represented the direction of the next generation of DeFi products. It could be said that Uniswap has made a critical step forward in the field of DEX. Uniswap has introduced the ability of position to support market makers to hold different positions in different price ranges, while for the management to position, or its tokenization, are all realized based on ERC-721, as it is obvious that ERC-20 is no longer able to make this.

Of course, this also brings about another question. As LP is no longer ERC-20, its potential liquidity has been significantly reduced. In terms of this, the explanation from Uniswap was that it was able to be achieved by peripheral agreements or through other partners. However, this method of peripheral implementation is definitely rigid and costly, the reason is that the ERC-721 does not support splitting or partial transfer, thus unable to allow the market makers to deal with the LP assets as flexibly as before. Meanwhile, the new added peripheral protocol will also increase the GAS consumption and reduce the trust.

From this point of view, the LP of Uniswap V3 cannot be said to be the optimal solution. If an asset agreement has both the descriptive capability of the ERC-721 and the quantitative attributes of the ERC-20, then actually, it can achieve a balance between the flexible positions and the liquidity. We have no idea why Uniswap did not continue this direction, but in order to achieve similar goals, we did take a step further on the asset agreement level and launched a brand new asset standard ERC-3525.

Mike Meng : Last October, we have proposed the idea of Digital Asset Vacancy in the article “What are digital assets”. At the time, I mentioned that there was no corresponding asset agreement in the blockchain to notes, and the most similar one was the ERC-721, which has high descriptive capability, but ERC-721 does not have quantitative attributes, which means that it is unable to be shared or split, which would lead to a lot of frictions in. The release of Uniswap V3 has just confirmed our point of view, as it is not a very good solution using the ERC-721 to directly describe the note assets, and ERC-3525 is a fundamental tool missing from the DeFi industry, it is the key to driving the industry towards DeFi 3.0.

Wang Wei: If we further ponder upon this question, the different price ranges in Uniswap V3 holds different functions of the positions. This is actually introducing the capability of “pricing market making”, which is quite similar to the capability to introduce “fixed lending” in the lending platform. Both of them allow the market participants to flexibly manage their asset agreements with the platform, except that one is making market in terms of a price range and rate, and the other is to make deposits or lending in terms of a certain time range and interest rate level. Furthermore, they are all similar to concepts such as “regularly unlock” in some investment agreements, the capabilities of which are not achievable through ERC-20.

To solve this kind of problem, the easiest way for people to understand is that the ERC-721 is one of the standard NFT models. But just like what we mentioned before, this kind of standard NFT model will inevitably bring about the inflexibility and high costs for asset handling, as well as the trust frictions generated when it is repackaged as the liquid asset, thus unable to realize its full potential to its significance of tokenization. Therefore, the ERC-3525 asset protocol we designed is not only able to describe the assets information from multiple dimensions and supports the differentiated operations and status changes of each asset, but it is also able to support free splits and mergers, hence to re-empower these assets to be shared, and enable the complex NFT-type financial products very flexible.

Ryan Chow: That’s right, Wei has opened up the perspectives. I’ve been thinking about what should the applications of DeFi in the next stage look like. As a matter of fact, starting from the logic that, the core of finance is to make cross-period exchanges of value, we are able to see a clear trajectory. The products of DeFi should be able to provide the users with a more flexible choice in periods, risks and benefits, and thus reduce the trading friction between both sides of the financial transaction, so as to facilitate a smoother transaction in the end.

Should DEX and derivatives provide market makers a richer option of risk-benefit combinations? Should the lending product provide the depositors a more flexible term option? Should an insurance product be able to provide the insurers the flexibility to choose the underlying and risk terms of coverage?

A better financial intermediary should be able to provide rich choices as it can reduce trade frictions, which leads to a smooth financial transaction. This logic is very clear. The products of DeFi should not just be stuck in the original infrastructure and mindset. It has already been fully proved that the code to replace the centralized trust is highly efficient. But for the code’s ability to describe the high-level financial services, it needs us to explore the problems and find a breakthrough solution.

We have always advocated from the perspective of notes to propose the innovation path of DeFi, in the future, there will be more and more projects trying to use the NFT. I have already seen this trend in many new products. As far as the direction of using the NFT to describe the contractual relationship between the user and platform, just like what Wang Wei has described, in terms of the suitability to the financial scene, the ERC-3525, has exceeded the ERC-721 and ERC-20, and it is also better than the ERC-1155 solution.

Mike Meng: The development of DeFi has finally made it to this stage, the note token will bring a brand-new model and new opportunities to all fields of DeFi and NFT. We have been groping for the term deposits and lending for the past six months since we have created the ERC-3525. And we did make a great breakthrough, we have developed a lending product to provide users with better term matching. However, in the end, we chose to bring a brand-new first-tier market release platform for the market from the perspective of the investment certificates(IC) . Zhiqiang, please tell us more details.

Ryan Chow: All right, in the end, here is the preview for our first ERC-3525 based innovative application — — the SOLV IC Market. We firmly believe that the ERC-3525 can bring significant changes to the industry. However, more needs to be done to prove this point. Focusing on ERC-3525’s characteristics of strong describing capability and being splitable, we have first selected a scene, which is not only interesting, but also able to give full play to the ERC-3525 characteristics, that is, the investor note release platform.

‘Solv Protocol, Reconstruct the Primary Market with NFT’

What does it mean? In the bull market, everyone wants to get the quota of the project as early as they can (generally, the quota of the project is required to lock up the position), however, in the case of share trading, the trading friction is tremendous, the most essential reason is that the share itself is a kind of complex contractual relationship, each share transfer, namely, the quota of private equity in purchasing and selling the project, needs a new contract signed through traditional legal means, and there are red tapes in the process, traps are everywhere.

Another point is that, in general, most people only want to trade part of their shares in the trading, not everyone wants to sell all the shares at once, and the splitting is another issue that is really troublesome. Taken together, the two pain points, i.e. the complex contractual relationships, and the demand for splitting the shares can be well solved by ERC-3525. Therefore, we will give priority to promoting such a platform, using the NFT notes to represent the Token during the lock-up period, and reconstructing the first-tier market in DeFi’s way. Through this, we hope to solve the pain points of the current market, meanwhile, also show the market our innovation.